Role

Senior Product Designer

Duration

12 months

Industry

Fintech

My Roles

UX Design

UI Design

UX Research

Team size

2 Product Designers

1 User Researcher

Business Case

NatWest strives to be the leading brand for early investing and financial literacy. With Rooster Money, (a top financial app for teens) boasting a strong customer base across age groups, we aim to leverage this advantage to capture the future banking market.

Research shows saving is a top priority for teens, and our focus is on enhancing their financial literacy and directing them towards meaningful, long-term financial products. Customers are likely to stay loyal to their bank longer than a serious romantic partner so feeling a strong emotional connection to their bank from an early age can promote lifetime customer value.

Research and Discovery

I conducted proof of concept research through

In 2023, earning and saving money are higher priority for kids than schoolwork, being nice to siblings or upping their recycling efforts.

The things they’re saving for range from days out to books and streaming subscriptions. However, video games and gaming accessories take the top spot as the most-saved-for item, accounting for the most goals created on the NatWest Rooster Money app in December with a target of over £191,000.

Having the ambition to save money is one thing - but sticking to it is something else. Data from NatWest Rooster Money from the last two years suggests that kids make far better progress towards their goals when they’re hot off the new year’s resolution buzz, highlighting why now is a key time for parents to engage with their child around money.

View Rooster Research

How do we help kids stick to their goals?

Our Hypothesis?

The key hurdle to kids achieving their financial goals was a combination of financial literacy and reminders from their loved ones.

If we could tie gift giving and recieving to key points in a child's saving journey in an enjoyable way this could encourage saving and sticking to their long term goal, improving financial literacy in teens and help gift givers and parents feel proud that their gifts are making an impact.

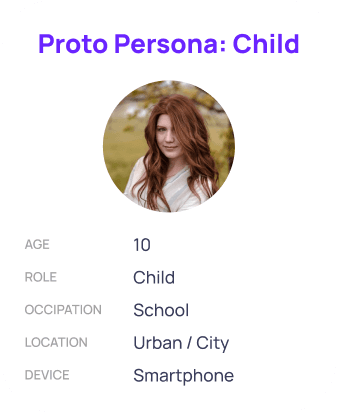

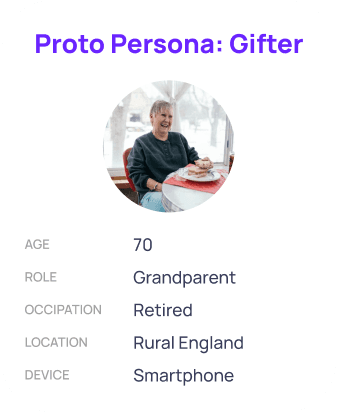

Getting to know Parent's and Kids motivations and pain points through research

7 one on one Interviews and 605 survey responses with NatWest customers and rival bank's customers of different age groups.

2x Parents: Father and Mother

4x Gift givers: Grandma, Aunt, Uncle and Grandma

1x Child

Expected outcomes:

Understand parents and kids motivations and fears are about long term savings goals?

What are current financial habits are around savings in the family and how is this encouraged?

Understand motivations around gifting, key family memories and people's experiences around this?

Parents

What they do?

2/2 interviews and 80% surveys Use basic savings account and set up the same for their kids instead of ISAs.

0/2 and 35% have regular financial literacy conversations with their children.

What they want?

2/2 and 90% want to have their savings accounts integrated with educational tools

2/2 and 80% wanted simplified access and a streamlined process.

Teens

What they do?

1/1 and 80% save only for immediate desires such as tech gadgets. With 0/1 and 15% saving for any long term goal.

1/1 and 75% have used a digital banking product and are familiar with how they work.

What they want?

1/1 and 100% wanted higher returns than average savings account but didn't understand how they could

1/1 and 90% wanted gamification or else they would find it boring.

Gifters

What they do?

4/4 interviews and 90% surveys leave it too late or and just give money or forget entirely.

3/4 and 65% believe that their gifts are not used regularly.

What they want?

4/4 and 85% want to be able to contribute to an account and give meaningful gifts.

3/4 and 77% want to humanise the financial experience as much as possible.

Defining our product goals with research

Brainstorming solution ideas. Using the 'How might we (HMW)' question and colloating all our research findings to define our key product goals that our MVP would further validate.

Money Mindset

Our financial mindset is shaped as young as 7, by showing the compounding effect overtime putting a little bit away can have compared to instant spending this can improve financial literacy.

Sustainability

Asking for money still carries a stigma, but directing gifts from family and friends towards investments, rather than disposable gift carries environmental benefits.

Leaving a Legacy

Connecting family memories in their life to the brand can help parents and gifters feel proud of the impact that they are having and can highlight that it inspired financially savvy decisions.

3 Personas. 3 Problems, 1 Integrated Product.

To understand how we could combine these product goals into 1 integrated product we crafted initial story maps and user flows and personas. We combined this with competitor analysis to see how other apps have brought about gifting gamification to bring meaningful experiences and how we can apply that to our product goals.

Painpoints:

Asking for money as a gift is not easy currently as its a sensitive topic. Tends to switch off to many financial and investing products.

Needs and Wants:

Control over the kind of learning and their kids developing with strong habits

Understanding of their sons finances through transparent benefits of different products.

Painpoints:

Financial learning can be boring and lack the incentives to engage. Want to be treated more 'grown up' and involved.

Needs and Wants:

Wants to play games and engage with character led digital experiences.

Want to feel their family memories can be accessed digitally as digital navtives.

Painpoints:

Often don't know the gifts children really want.

Doesn't like overly complex digital processes

Needs and Wants

Want to make an impact and leave a legacy to help their grandchildren grow.

Want to see what are their child's short term and long term goals.

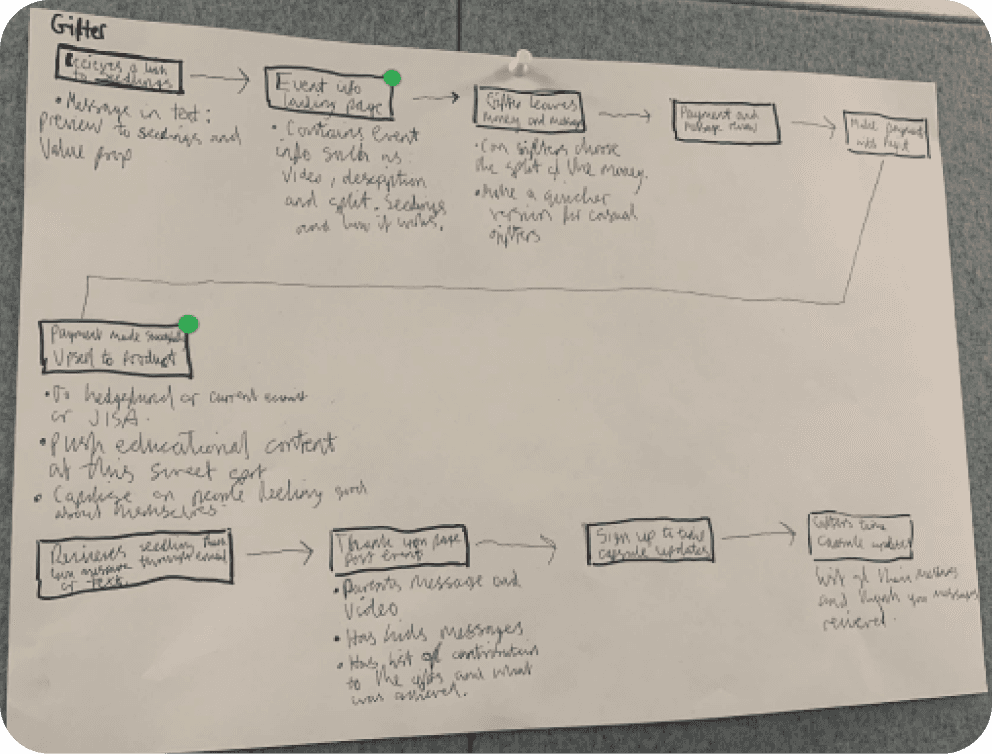

Mapping the User's flow

Getting the key parts of the journey down allowed me to identify where key emotional triggers can arrive and how we can identify key challenges and pain points along the way for our users.

3 Interlinked journeys emerged

We brought together the user journey's know full well that different priorities existed for the different user groups.

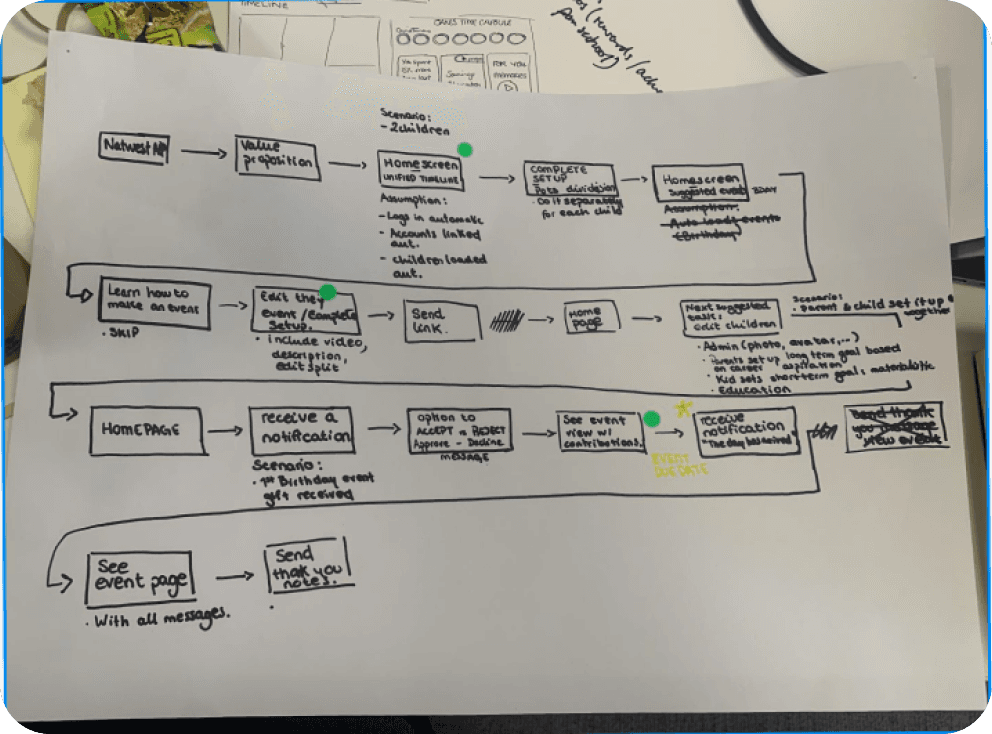

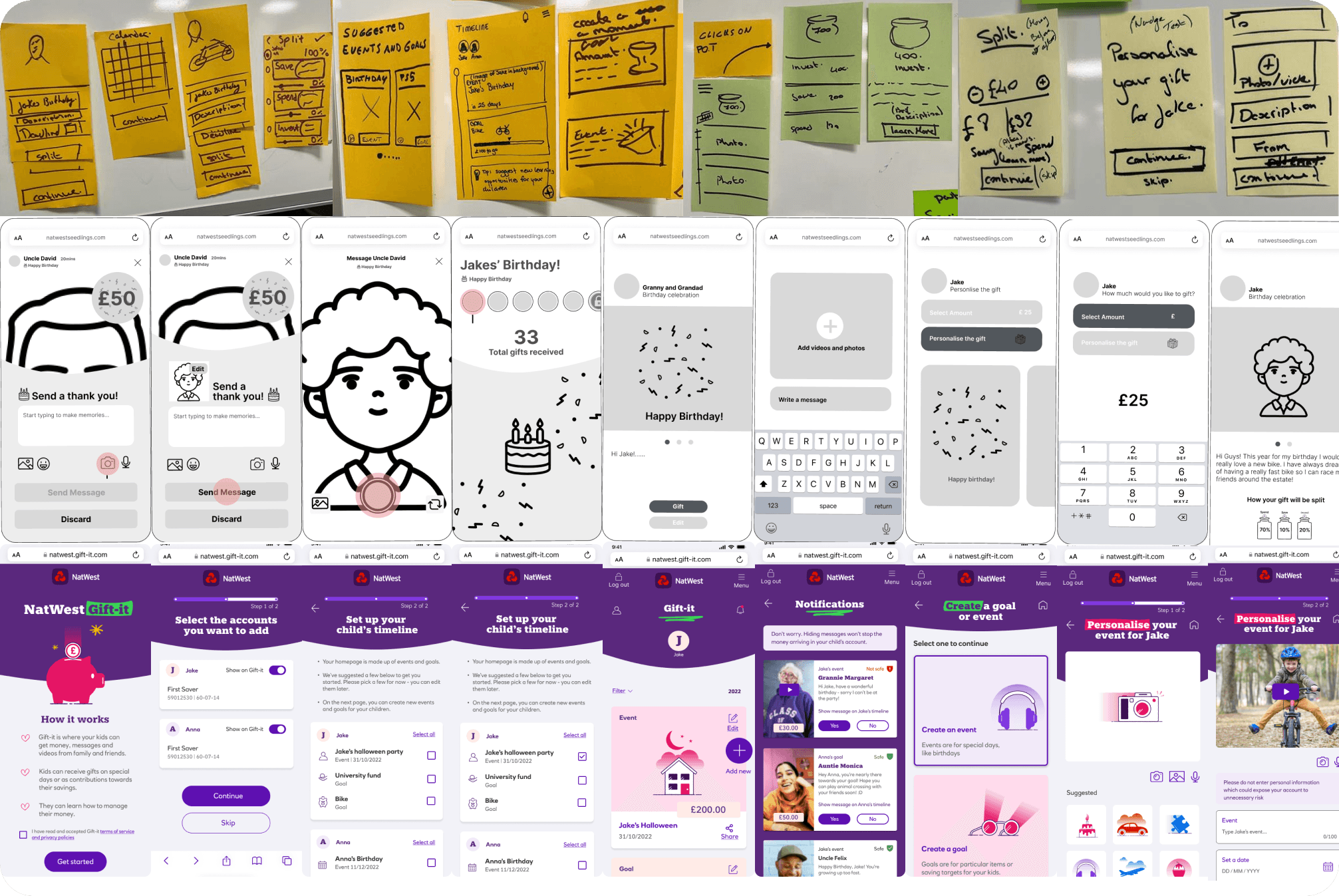

We turned to sketching

Putting it down on paper

Sketching is a great way to conceptualise different ideas and flows quickly to rapidly iterate at this stage to what journey's could make sense. We tested these internally at a very early stage to see what flows and journeys made sense and solved our key product goals.

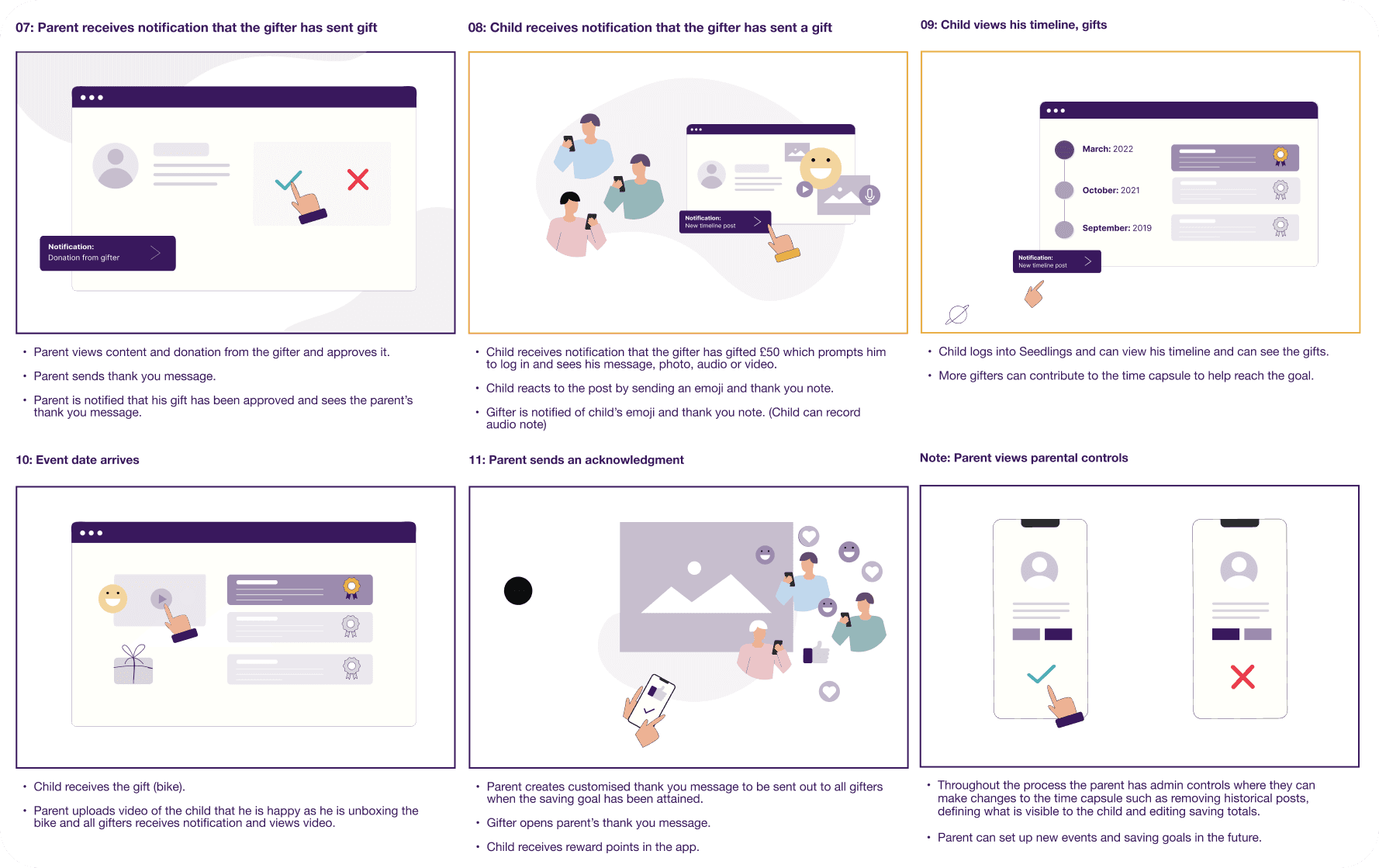

Scaling up the fidelity

Once I had my ideas consolidated we put them into low fideflity to see how the journey's made sense. The benefit of this is we didn't need to apply branding when converting our skteches into mobile screens. I wanted to test the quality of the ideas and journeys primarily.

Once these were established we could move to focusing on how I could apply our design system to make the journey and experience really pop.

Assume nothing, test everything

Usability Testing was underway.

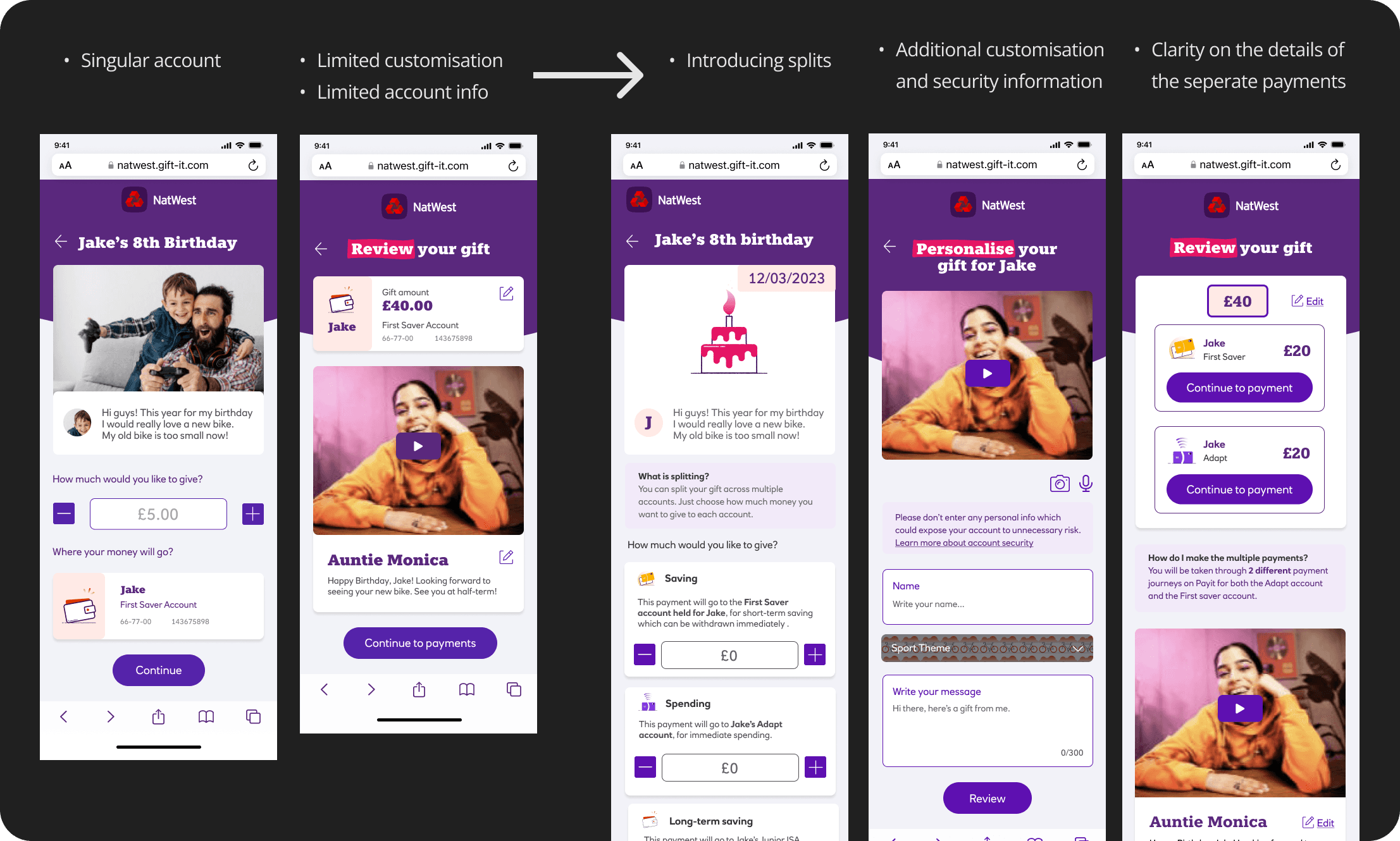

We wanted to test the premise of whether the concept resonated well and the key product goals are understood. Incentivising splitting and testing the setup could be done easily whilst conveying the key values of the app. We wanted to dial down the key motivation and focus on how gifting could work as a concept before introducing financial literacy and education into the application.

12 total test participants. Moderated remote tests.

4 Gifters adults who have experienced gifting money digitally before.

Parents

4 Parents with young children

Set up their Children and the correct accounts easily?

How parents responded / Event / Goal custom event set up.

`Could parents understand the difference between the purpose of the different accounts.

How did adding customised photo / video content test?

Managing gifter's content?

Kids

4 Children aged 6-12

How exciting is the gift opening process for kids?

Testing the interest in sending thank you messages and personalisation

How well did different types of content (images, videos, audio resonate with the child)

Does notion of saving make sense and desire for long term goals clear?

Interest in education.

Gifters

4 Gifters adults who have experienced gifting money digitally before.

Testing the emotions of saving up for a goal or gifting to an event and what their contribution could achieve.

Tested thoughts around giving part of the money to savings and understanding of the different account available.

Testing how many chose to give their own images and customisation

Test Summary and findings

Parents

4/4 Wanted more visibility over the accounts involved,

3/4 Didn't want to add pre made events and goals and wanted to set up their own events

4/4 Wanted to see more educational content available relevant to each of their children

3/4 Found the gift reviewal process and adding of events hard to find. This included aspects of the nav such as child selection.

Kids

4/4 Children found generic imagery unexciting. The scrolling format tested negatively and lacked enough surprise.

3/4 Had no interest in saving the money or lacked knowledge of benefits showing opportunity to involve education at this point.

2/4 Ignored sending a personalised thank you message.

3/4 Would skip messages without personalised images and dropped engagement with app.

Gifters

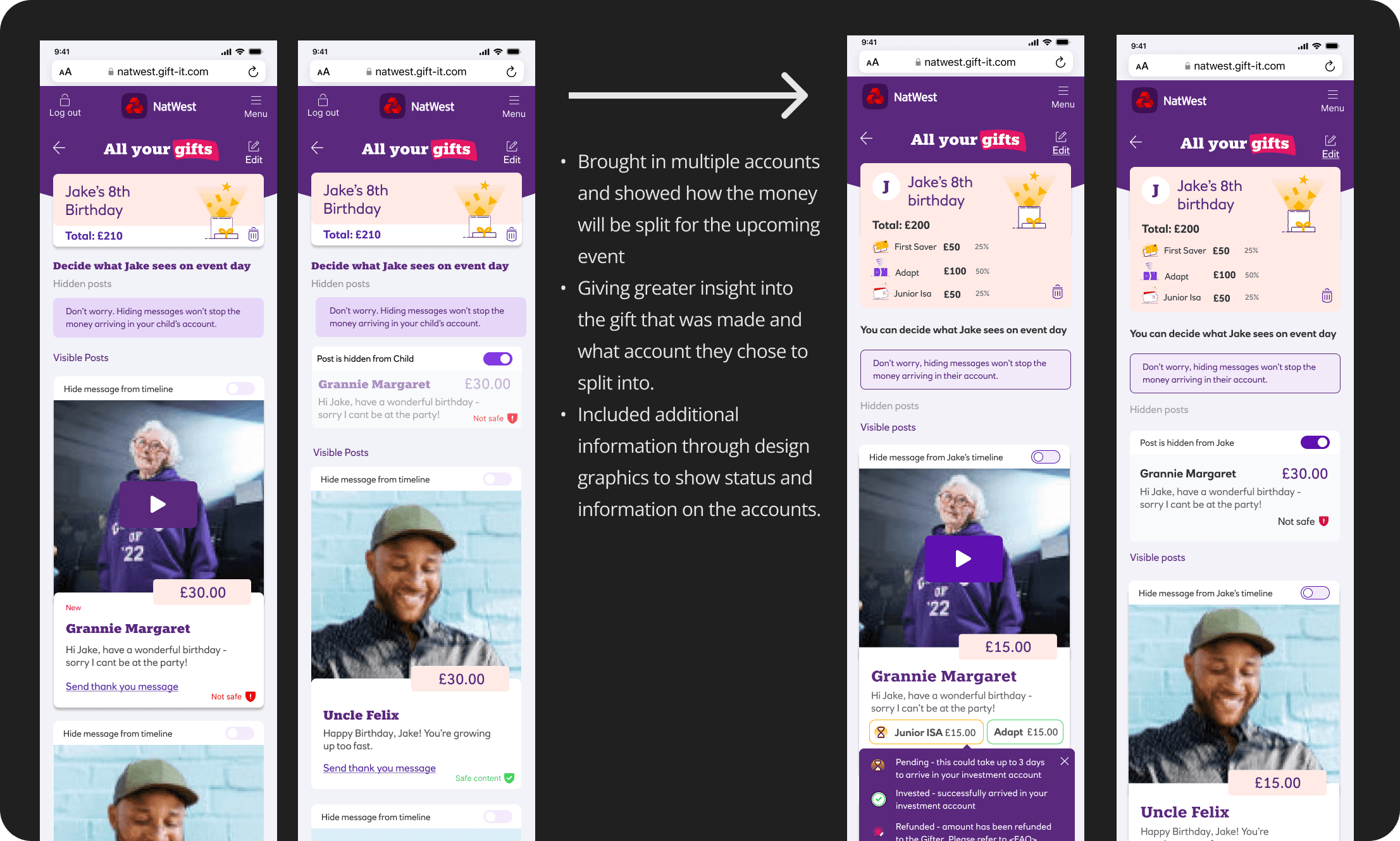

2/4 Felt they needed to add their own photo or video to make it special of them they wanted more customisation and uniqueness to their gift.

3/4 Wanted more control and transparency over where the money was sent

3/4 Wanted more information on the premise of the application and why to use this over sending the money directly.

2/4 were willing for the process to be longer in order to feel security with the application.

Next wave to test:

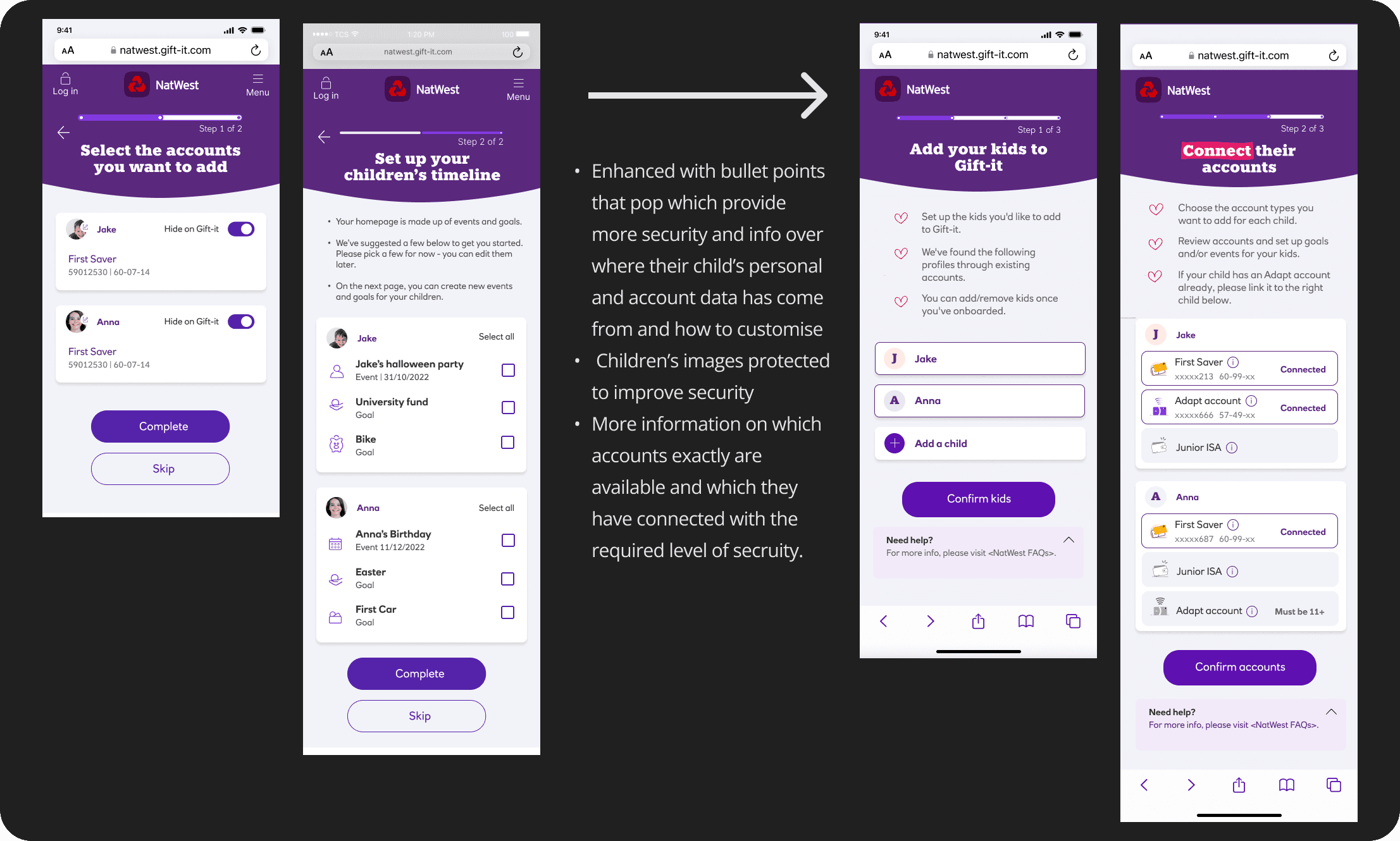

Providing user with more clarity upfront on security of the app especially around use of personal photos and account information.

Creating a clearer and more flexibly processes of setting up and minotring events and goals

Integrating education to review and building this into a cleaner interface.

Next wave to test:

Focus on addressing current issues on engagement and excitement of experience.

Intergrating further mystery and ability to speed up boring parts of the experience.

Introducing financial education as part of the gifting process and make the education around splitting more prominent.

Next wave to test:

Balance for users that want to customise and also for those that want to complete the journey quickly.

Take more time to give users security and transparency on where the money is going.

Show more transparency over saving money's impact and how this spend is making an impact with information around different accounts.

Reflecting and re-engineering.

Learning a lot from the usability test we redeployed our energy to ideating and sketching to face the problems head on. We knew that we had to go back to sketching to engineer these journey's to dial in and focus in on our key user needs whilst prioritising our product goals.

Below you can see the updated and final prototypes that addressed the issues.

The solution

Simplicity

I applied the changes and brought the design to life and brought the new design back to users collected from he same sample group.

We had identified the pain points that were acting as barriers to our key product goals of improving financial literacy, sustainability and leaving a legacy. By testing how the concept of gifting resonated with users and then once validated how to provide that in a way that caters for all our customers needs and helps keep engagement and user satisfaction high.

Results

Improvements in paid memberships

I applied the changes and brought the design to life and brought the new design back to users collected from he same sample group.

We had identified the pain points that were acting as barriers to our key product goals of improving financial literacy, sustainability and leaving a legacy. By testing how the concept of gifting resonated with users and then once validated how to provide that in a way that caters for all our customers needs and helps keep engagement and user satisfaction high.

Applying the brand to match the theme.

A fun and engageing brand to match the energy of the app

If you haven't already seen my case study on how I worked on rebuilding the NatWest design system you can view by clicking here.

After a significant redesign focused on bringing NatWest in the modern era and giving the brand a youth focused appeal. The new design system had elements drawing from Rooster to express the design system to meet the product goals.

Reflections and Learnings

Keep it simple

Focusing on improving the simplicity of the message for kids. Keep the benefits clear on

We should have focused more attention on the child's experience as the primary product goal and have all other experiences coming out of that.

Relying too much on oversimplied personas based on too many assumptions rather than focusing on the core user need of the product.

Plans are in place to integrate AI to improve the excitement of this experience. You could select your favourite character or celebrity and receive gifts from these people.

After a significant redesign focused on bringing NatWest in the modern era and giving the brand a youth focused appeal. The new design system had elements drawing from Rooster to express the design system to meet the product goals.